IUL INTRODUCTION

Understanding Indexed Universal Life Insurance

Learn how Indexed Universal Life (IUL) Insurance combines life insurance protection with tax-advantaged growth potential, offering a unique solution for both family security and wealth building.

Are you looking for a way to protect your family’s financial future while also building wealth that you can access during your lifetime? Traditional investment accounts come with market risks, while basic life insurance only provides death benefits. What if there was a solution that offered both protection and growth potential? Enter Indexed Universal Life (IUL) insurance – a flexible financial tool that’s gaining attention from forward-thinking financial advisors, planners, and tax strategists.

FREE DOWNLOAD

The Ultimate Guide to Indexed Universal Life Insurance

Unlock the secrets of IUL insurance with this comprehensive guide. Discover how to leverage its unique benefits for lifelong protection, cash value growth, and tax advantages. Download now and start planning for a secure financial future!

Understanding IUL Insurance: The Basics

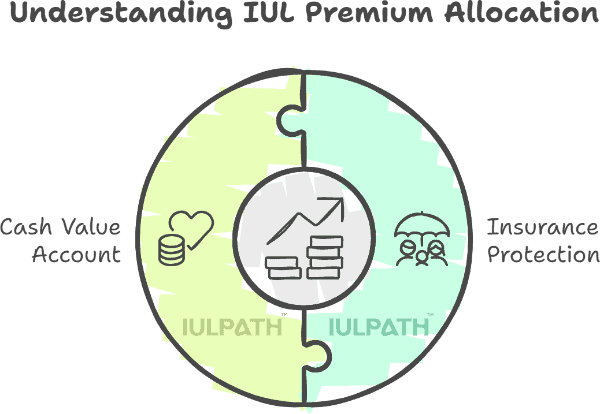

Indexed Universal Life insurance combines permanent life insurance protection with a cash value component that can grow based on market index performance. Think of it as a hybrid financial vehicle – part life insurance, part investment account, but with unique features that set it apart from both (see below).

Here’s how it works: When you pay your IUL premium, it’s divided between your insurance protection and your cash value account. The cash value portion has the potential to grow over time, and you can access it during your lifetime for any purpose – from supplementing retirement to handling emergencies.

What Makes IUL Insurance Different from Traditional Life Insurance?

Most people are familiar with basic life insurance – a straightforward way to provide for loved ones after you’re gone. IUL insurance takes this core concept and enhances it by adding features that can benefit you during your lifetime. It combines death benefit protection with the potential for cash value growth tied to market performance, but – and here’s where it gets interesting – without direct market risk and with the ability to access your cash value account when you need to.

Term Life Insurance vs. IUL

- Term Life: Pure death benefit protection for a specific period (like 20 years)

- IUL: Permanent protection plus cash value growth potential plus access to cash value account

Whole Life vs. IUL

- Whole Life: Guaranteed death benefit and cash value growth at fixed rates

- IUL: Potential for higher returns while maintaining downside protection

Key Features That Make IUL's Unique

IUL insurance builds upon the foundation of traditional life insurance by adding features that work for you while you’re living. It maintains the essential death benefit protection while offering unique capabilities that can help you meet multiple financial goals.

1. Market-Linked Growth Potential

- Cash value can grow based on market index performance

- Potential for higher returns than traditional whole life insurance

- Built-in protection against market losses

2. Flexibility

- Adjust premium payments (within limits)

- Access cash value when needed

- Modify death benefit as your needs change

3. Tax Advantages

- Tax-deferred growth of cash value

- Tax-free access through policy loans

- Tax-free death benefit for beneficiaries

Benefits of IUL Insurance

As you consider an IUL policy, it’s important to understand what sets it apart from other financial tools and why so many savvy savers are excited about it. The combination of protection and growth potential creates unique advantages that can help address multiple financial goals simultaneously.

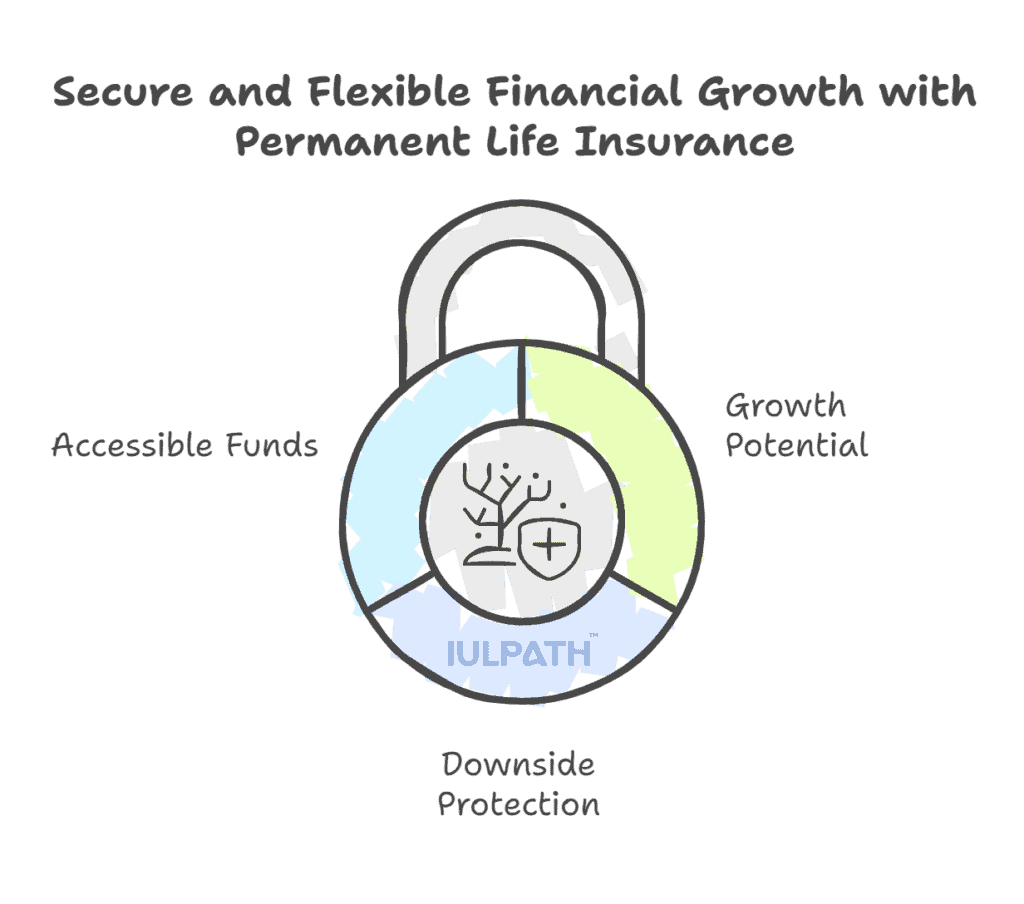

1. Protection with Growth Potential

You get permanent life insurance coverage while having the opportunity to build tax-advantaged cash value based on market index performance.

2. Downside Protection

Your cash value has a guaranteed floor (typically 0%), meaning you won’t lose money when markets decline.

3. Access When You Need It

Unlike traditional retirement accounts, you can access your cash value at any time, without penalties for early withdrawal.

Important IUL Considerations

Like any sophisticated financial tool, IUL comes with important considerations you need to understand. Just as a high-performance car requires more attention than a basic sedan, an IUL policy needs proper management and understanding to perform at its best, which is why we recommend connecting with a licensed IUL insurance agent to see if an IUL policy is right for you.

1. Cost Structure

- Higher initial costs than term insurance

- Insurance costs increase as you age

- Policy fees and charges can impact cash value growth

- Need to maintain adequate funding to keep policy in force

2. Market Participation Limitations

- Cap rates limit your upside potential

- Insurance company can adjust cap rates

- You don’t receive dividend payments from indexes

- Market volatility can affect year-to-year performance

3. Policy Management

- Requires active monitoring and management

- Loans must be managed carefully to avoid policy lapse

- Missing premium payments can affect policy performance

- Need to review and adjust strategy periodically

4. Long-Term Commitment

- Best results typically seen after 10-15 years

- Early surrender can result in significant fees

- Not ideal for short-term planning

- Requires consistent premium payments

Is an IUL Policy Right For You?

An IUL is best for savers and protectors who:

- Want permanent life insurance protection

- Are looking for tax-advantaged growth potential

- Value flexibility to access their savings tax and penalty-free

- Have maxed out or don't have access to other retirement accounts

- Want protection against market downturns

Real-World Example

Let’s look at how one family incorporated IUL insurance into their financial plan to address multiple goals simultaneously.

Real-World Example

How People Are Using IUL Plans

Sarah and Michael were at a crossroads in their financial planning. Like many successful professionals in their mid-40s, they had built a solid foundation – good careers, a comfortable home, and two children heading toward college years. While they had done the basics right with term life insurance and regular 401(k) contributions, something was keeping them up at night: balancing protection for their family with the need to build more tax-efficient wealth for the future.

Their financial advisor introduced them to IUL as a potential solution. With a combined income of $280,000, they had maxed out their retirement accounts but wanted more tax-advantaged growth potential. They also knew their $500,000 each in term life insurance would eventually expire, leaving them without coverage in their later years.

After careful consideration, they implemented an IUL strategy with a $1 million death benefit and $2,000 monthly premium. The policy was designed to balance protection with cash value accumulation, giving them flexibility for future needs like college funding or supplemental retirement income.

Five years later, their policy has performed as designed. They’ve paid $120,000 in total premiums and built $135,000 in cash value, with $108,000 available for tax-free loans if needed. Most importantly, they’ve secured permanent life insurance protection while creating a tax-efficient asset they can access during their lifetime.

“What sold us,” Sarah explains, “was the combination of security and flexibility. We’re protected if something happens, but we’re also building something we can use for whatever life brings our way.”

Frequently Asked Questions

IUL insurance can seem complex at first, but understanding a few key points can help you grasp its potential role in your financial strategy. Here are answers to the questions we hear most often from people considering IUL insurance.

While both options provide market-linked growth potential, IUL offers unique features that set it apart from direct stock market investing. With IUL, your cash value is protected against market losses through a guaranteed floor rate (typically 0%). However, there's also a cap on your maximum returns (often 8-13%). Unlike stock market investing, IUL provides tax-advantaged growth, tax-free access through loans, and a death benefit for your beneficiaries. The trade-off is that you won't participate in dividends and your upside potential is limited by caps, but you gain protection against market downturns and valuable tax advantages.

Have more questions? Schedule a call with a licensed IUL insurance agent.

Most IUL policies require a medical exam as part of the underwriting process, which helps the insurance company accurately assess risk and determine your premium rates. The exam typically includes basic health measurements (height, weight, blood pressure), blood and urine tests, and a review of your medical history. Some carriers offer "simplified issue" policies that don't require an exam, but these generally have lower coverage limits and higher premiums. The healthier you are, the better your rates will be, so the medical exam can work in your favor if you're in good health.

Have more questions? Schedule a call with a licensed IUL agent.

The cost of an IUL policy depends on several factors: your age, health, coverage amount, and how you structure the policy. A typical policy might start at $200-300 monthly for basic coverage, but can range much higher depending on your goals. The premium includes three main components: the cost of insurance (which increases with age), policy fees and charges, and the remainder that goes to your cash value. It's important to understand that early years of the policy have higher relative costs, while cash value typically grows more significantly in later years. Your financial professional can help structure premiums to align with your goals and budget. Talk to an IUL expert today.

Have more questions? Schedule a call with a licensed IUL agent.

While your cash value has downside protection against market losses, there are several scenarios where you could lose money in an IUL policy. First, if you surrender the policy in the early years, you'll face surrender charges that could result in getting back less than you've paid in. Second, if you take loans from your policy and don't manage them properly, accumulated loan interest could cause your policy to lapse, potentially triggering tax consequences. Third, if you don't maintain adequate premium payments, policy costs could erode your cash value over time. That's why it's essential to view IUL as a long-term strategy and work with a financial professional to properly structure and manage your policy.

Have more questions? Schedule a call with a licensed IUL agent.

Your ability to access cash value develops over time. In the early years (typically 1-10), surrender charges apply if you withdraw money directly. However, you can usually access your cash value through policy loans after the first few years. These loans are tax-free as long as the policy remains in force, and you can typically borrow up to 90-95% of your cash value. Keep in mind that loans accrue interest and reduce your death benefit until repaid. Some policies also offer other features like zero-net-cost loans or preferred loan rates after a certain period. It's crucial to structure any loans properly to maintain the policy's tax advantages and prevent policy lapse.

Have more questions? Schedule a call with a licensed IUL agent.

IUL can be an effective complement to traditional retirement planning, particularly for those who have maxed out other tax-advantaged options or want more flexibility. The key advantages for retirement planning include tax-deferred growth, tax-free access to cash value through loans, no required minimum distributions, and no contribution limits. However, IUL works best as part of a broader strategy rather than a standalone retirement solution. The policy needs to be properly structured and funded to optimize its retirement planning benefits. Higher early premiums typically provide better long-term results for retirement income purposes. Your financial professional can help model different scenarios to show how IUL might fit into your retirement strategy.

Have more questions? Schedule a call with a licensed IUL agent.

Determining if IUL fits your financial strategy requires careful consideration of several factors and must be done by speaking with a licensed IUL professional. First, assess your needs for both life insurance protection and tax-advantaged growth potential. Second, evaluate your financial stability and ability to commit to long-term premium payments. Third, consider your risk tolerance and comfort with market-linked returns that have both caps and floors. IUL typically works best for people who: want permanent life insurance protection, have maxed out other tax-advantaged accounts, can commit to regular premium payments for 10+ years, value downside protection over maximum returns, and want flexibility in their financial strategy. A financial professional can help analyze your specific situation and determine if IUL aligns with your goals.

Have more questions? Schedule a call with a licensed IUL insurance professional.

Next Steps

Learning about IUL insurance is just the beginning of your journey. Now it’s time to explore whether this unique financial tool aligns with your specific situation and goals.

The Ultimate Guide to Indexed Universal Life Insurance

Unlock the secrets of IUL insurance with this comprehensive guide.